In our previous blog we focused on expenses and how we can box them to make sorting easier. We now looking at the savings.

Many of us suffer from flawed mental accounting, we believe that

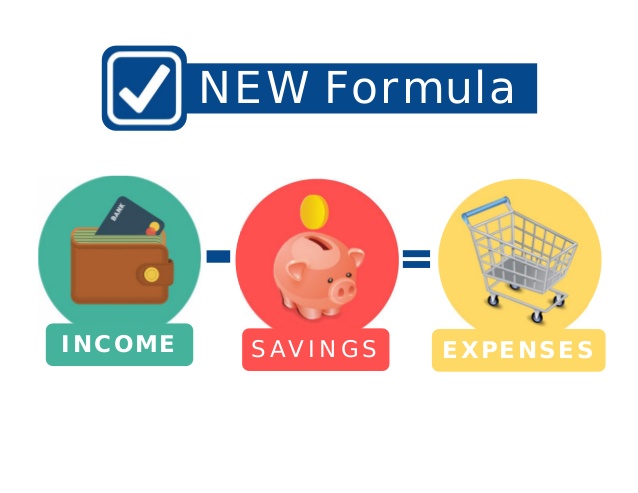

Income – Expenses = Savings

Which means we plan to save with whatever income we have left, which never happens. Very few people manage to have more money than month usually there is a lot more month than money. We need to rethink our mental accounting to

Income – Savings = Expenses

We need to save first to ensure we achieve our goals then adjust our lifestyles to live with what we have left.

An Athlete, Entrepreneur and Parent

What does an athlete, entrepreneur and a parent trying to get their teenager through school have in common? They all have clearly defined goals and a plan they work towards. A common thread for all of them is that things almost never go according to plan.

Injury, economic downswings and the onset of puberty can all derail even the most resolute regimes and plans. This challenge doesn’t stop them from achieving their goals. Their mindset is always set on their goals and during these challenging times, they reflect, adapt and redraw their plan.

An athlete’s long term goal may be to win a gold medal or break a record. In order to achieve this they would need to set smaller milestones and goals depending on how far they are from their goal. These smaller goals are just as important because if we cannot achieve them there is no hope we can succeed in the long term.

We need to take the same approach with our savings. We generally divide Financial goals in three categories short, medium and long term goals. Placing a time-frame on your savings goals helps put it into perspective what you need to be saving and the time-frame you need to get there.

Short-term Goals

0 – 12 months

Depending on the amount or the cost, these goals could be things like tuition for next year, car service and tyres, replacing household appliances or maybe a holiday (depending on where you are going). Some short term goals often repeat each year like a car service.

For many of us the cost of servicing a vehicle or any of our short-term goal is generally not something we can pay out of our monthly budget. Which means with a little planning we can save for them.

Medium-term Goals

3 – 5 years

Goals that will take longer to achieve and usually we need to remind ourselves from time to time in order to stay focused.

Could be things like, a deposit for a house, buying a car, perhaps an overseas holiday, building up an emergency fund or being debt free (with high interest rates often paying off debt is an excellent form of saving).

These goals require us to put our head down a bit, we do not need to evaluate these goals monthly but rather quarterly or we even suggest annually. A unit trust is an excellent vehicle for saving for the medium term as you can set up a debit order monthly and with the right product you can have flexibility to increase or decrease contributions with ease.

Long-term Goals

5+ years

Goals that take so long most of us struggle to even imagine the end result. These goals are saving for retirement, your child’s education, a bigger house or a long term travelling holiday.

Quite often these goals are our big talking points and can generate the biggest concerns but we don’t always realise we need to reach our smaller milestones in order to reach our long term ones.

When looking at our goals we tend to either lack long term perspective, over prioritising the short term. Or we tend to only have a retirement plan in place but no short term savings plan.

Having a financial advisor help you structure your goals provides objectivity and accountability. Make sure they are independent

If reading this has sparked some interest and you have some questions get in touch and let us know.

At Growmatter we have 4 elements, we want to Live Trust Grow Matter.