Following on from our Money Management 101 Intro we now need to get to grips with our expenses. We need to group our expenses. We can call these groups boxes, buckets or categories, whichever feels more natural.

We prefer to use the term boxes because generally boxes have lids and by design boxes contain things. Expenses are definitely something we want to contain and keep a lid on.

Expenses are broken down into three main boxes Fixed, Variable and Fixed Variable. There is a 4th box we call Smart Expenses but more on this later.

Fixed expense

Our month-to-month payments that remain the same regardless of changes, these will be bond repayments or rent, cell phone accounts or car repayments. If you signed a gym contract for R200 p/m, it will remain R200 p/m each month until an increase. You will not suddenly pay R600 one month and then R200 the next, the amount that is agreed upon is fixed.

The definition of fixed expenses although similar might not be the same for everyone. Some households treat certain expenses as fixed for example a cell phone account. Every month they purchase the same amount of minutes and data and if they run out then so be it. For some people, this is not functional and they would categorise their cell phone as a variable expense.

Giving or gifts is another example of how definitions may differ for each person. Some people have a fixed monthly amount they give to charities, churches or support programs. While some people may give varying amounts each month.

We have a Money Management process called MoneyMatters. With predefined groups it can help get any body started.

Variable Expense

These expenses are calculated based on your consumption or use. For example clothing, entertainment, doctors visit, luxuries etc

These figures are likely to fluctuate month to month however we still put an amount for each of these items as a basis for how much money you are spending. We see these amounts as goals in our Money plan, being under is achieving our goal. If we are over it means we need to find income from another box to make things work.

If we don’t plan for some of our bigger expenses like car tyres, appliances and household maintenance it could end up putting us under pressure. Potentially forcing us to loan money, go into overdraft or live on our credit card. These all come at a costly interest premium and could be avoided through simple money management steps. Allocating some funds towards the unexpected expenses bucket can help with this. This we call our emergency fund and can make a huge difference when experiencing speed bumps.

Fixed Variable Expense

Our last core category of expenses. These are expenses that we simply must have but they fluctuate each month. Things like petrol, electricity, water and food. Petrol is a good example of the importance of planning. If you are planning a weekend away you need to allocate more to it.

Some of these items vary more than others but they are important and in general if you monitor your spending you will notice these amounts are fairly consistent.

The crux of dealing with expenses is about discipline, you put a plan in place and then you need to work towards it.

Smart Expenses

These are expenses that have a stipulated amount that you should pay but you choose to pay more for a short-term or even long-term reward. For example putting more into your bond, and paying more into your clothing account to clear debt quicker and save on interest. Another example is paying an early bird fee for school or studies to get a bigger discount.

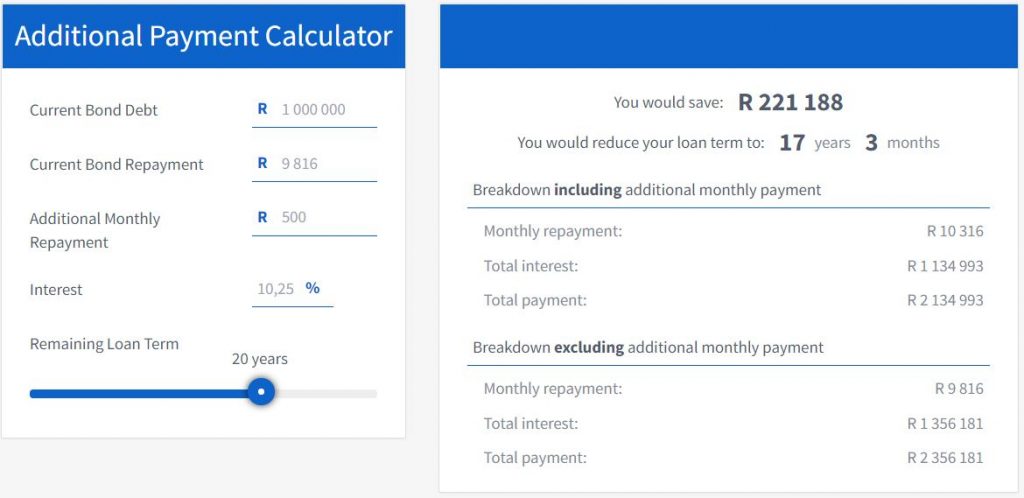

Using a bond example of R 1 million over 20 years, below you can see if you pay R500 more on your bond each month you will pay your bond off almost 3 years sooner and also save over R220 000 in interest.

Not sure about you but I could certainly use R220 000 more than the bank can.

We are pro-saving, but we are even more pro-debt-free living. We cannot advise someone to save when they are sitting on a mountain of high-interest debt like short-term loans, credit card debt and overdrafts. Clearing your debt should be your immediate goal.

There are income tax benefits to things like retirement savings which have the potential to gain above the interest you are paying. With that in mind, the gains almost never outweigh the high interest on a credit card or overdraft.

Remember compound interest works both ways “Those who understand it earn it… Those who don’t pay it”

If you are keen to start your money management plan contact us

Live. Trust. Grow. Matter.